• Expenses Incurred by Employees on Behalf of Employers

Disbursements and Reimbursements

Reimbursements and disbursements must be included in e-Invoices.

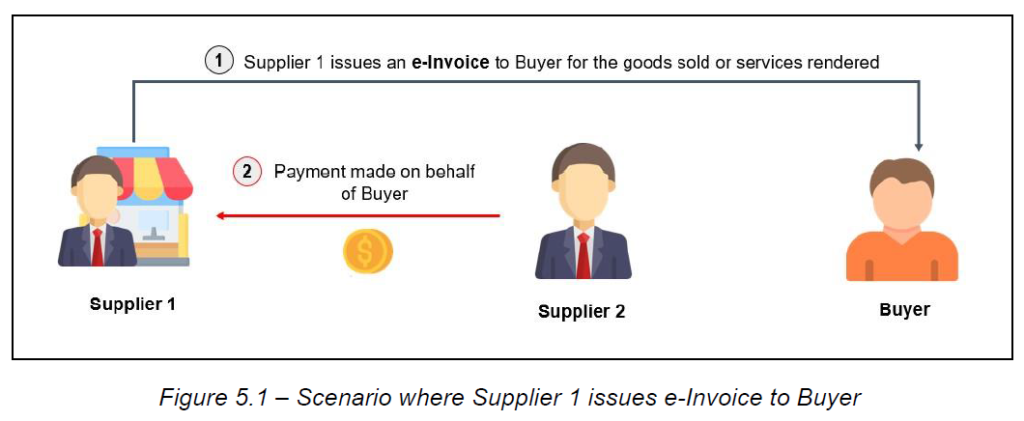

Scenario 1: Supplier 1 issues e-Invoice to Buyer

Step 1:

Supplier 2 entered into an agreement with Buyer for supply of goods or provision of services. As part of the arrangement, Supplier 2 will make payment on behalf of Buyer to settle any expenses incurred during the contract period.

Step 2:

Upon concluding a sale or transaction, Supplier 1 will issue an e-Invoice directly to the Buyer.

Step 3:

Supplier 2 will make payment on behalf of Buyer to Supplier 1 to settle the outstanding amount. Supplier 1 will issue payment proof to Supplier 2 for the settlement.

Step 4:

Supplier 2 will issue an e-Invoice to the Buyer for the goods supplied or services rendered by Supplier 2 to Buyer (the process of issuing e-Invoice is similar to Step 2 above). Supplier 2 should neither include the payment made on behalf of Buyer in Supplier 2’s e-Invoice nor issue an additional e-Invoice for it.

Step 5:

Supplier 2 provides payment proof to the Buyer to recover the payment made to Supplier 1 on behalf of the Buyer.

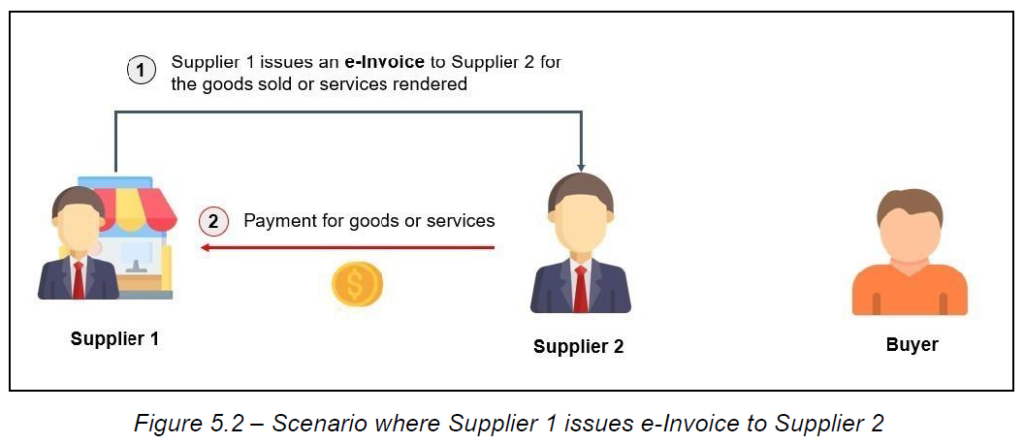

Scenario 2: Supplier 1 issues e-Invoice to Supplier 2

Step 1:

Supplier 2 entered into an agreement with Buyer for supply of goods or provision of services. As part of the arrangement, Supplier 2 will make payment on behalf of Buyer to settle any expenses incurred during the contract period.

Step 2:

Upon concluding a sale or transaction, Supplier 1 will issue an e-Invoice to Supplier 2.

Step 3:

Supplier 2 will make payment to Supplier 1. Supplier 1 will issue payment proof to Supplier 2 for the settlement.

Step 4:

Supplier 2 will issue an e-Invoice to the Buyer (similar as per Step 2 above) to record the amount incurred on behalf of Buyer (e.g., disbursement / reimbursement) alongside with the goods sold or service rendered by Supplier 2, which will be presented as separate line items in the e-Invoice.

Employment Perquisites and Benefits

Employees may receive benefits in cash or kind, such as utility bill payments, club memberships, gym memberships, professional subscriptions, and allowances (e.g., travel, petrol, meal).

Employees must submit expense claims with supporting documents (e.g., bills, receipts, invoices) to their employers.

With e-Invoice implementation, employees should request e-Invoices issued to their employer as proof of expense. However, IRBM allows concessions where e-Invoices can be issued in the employee’s name or existing documentation can be used for tax purposes.

For payments to foreign suppliers, no self-billed e-Invoice is required, and foreign receipts/bills are accepted as proof of expense.

Expenses Incurred by Employees on Behalf of Employers

Employees may incur expenses on behalf of their employer, such as accommodation, toll, mileage, parking, and telecommunication expenses.

Similar to benefits, employees must provide supporting documents for expense claims.

IRBM allows e-Invoices to be issued in the employee’s name or existing documentation for tax purposes, especially for overseas expenses.

Steps for Expense Claims:

Employees should confirm with suppliers if e-Invoices can be issued in the employer’s name.

If not possible, e-Invoices can be issued in the employee’s name.*

* Note: that this exception will only be applicable if the employer is able to prove that the employee is acting on the employer’s behalf in incurring the expenses.

Employees pay upon receiving validated e-Invoices and submit them as supporting documents for expense claims.