The e-commerce platform provider is responsible for issuing e-Invoices or receipts to consumers for transactions concluded through the platform. Merchants are not required to issue e-Invoices or receipts.

If the buyer does not request an e-Invoice, the platform provider can issue a consolidated e-Invoice for multiple transactions, with a specific classification code indicating e-commerce transactions.

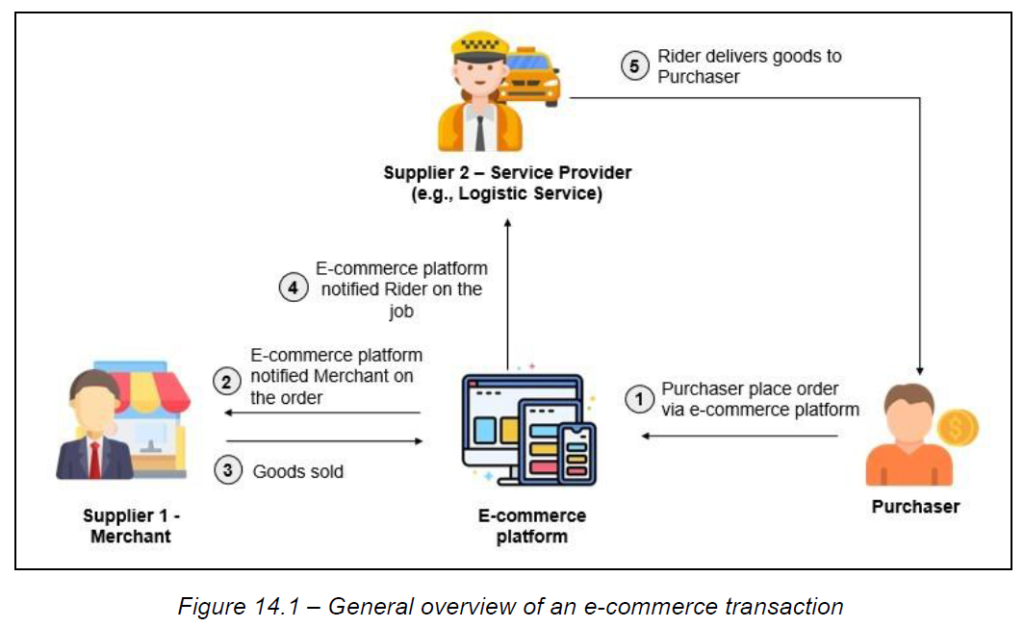

Recording Income for Merchants/Service Providers:

The e-commerce platform provider must issue self-billed e-Invoices to record income generated by merchants or service providers (e.g., logistics providers) from transactions on the platform.

The frequency of self-billed e-Invoice issuance should align with the platform’s current billing practices.

Consolidated e-Invoices are not allowed for recording merchant income from e-commerce transactions. Instead, self-billed e-Invoices must be issued.

Timing of e-Invoice Issuance:

The platform provider can follow current billing arrangements, issuing draft/proforma invoices to merchants. Only the final e-Invoice needs to be submitted to IRBM for validation.

Charges Imposed by E-commerce Platforms:

The platform provider must issue e-Invoices for charges imposed on merchants or service providers for using the platform. The issuance frequency should follow current practices.

Tax Identification Number (TIN) for Foreign Suppliers:

If a foreign supplier does not have or provide a TIN, the general TIN “EI00000000030” can be used in self-billed e-Invoices.

Refunds for Returned Goods:

A refund note e-Invoice must be issued by the platform provider to record refunds for returned goods.

Consolidated e-Invoice for E-commerce and Brick-and-Mortar Transactions:

It is not advisable to include e-commerce transactions in the same consolidated e-Invoice as brick-and-mortar store transactions due to differences in transaction flow and classification.