Post Your Ad

Home

E-Invoice Info

Login or Register

More Info

Refund or Return Policy

Service Delivery Policy

Terms & Conditions

Email Address

[email protected]

Home

E-Invoice Info

Login or Register

More Info

Refund or Return Policy

Service Delivery Policy

Terms & Conditions

Log In

Register

Post Your Ad

Register now and list your ad for FREE!

- Tutorial (how to post)

How-03: How does e-invoicing work?

Self-billed e-Invoices

General E-Invoice Issuance:

Typically, the supplier issues an e-Invoice to recognize income and record purchases.

However, in certain circumstances, the buyer is required to issue a self-billed e-Invoice.

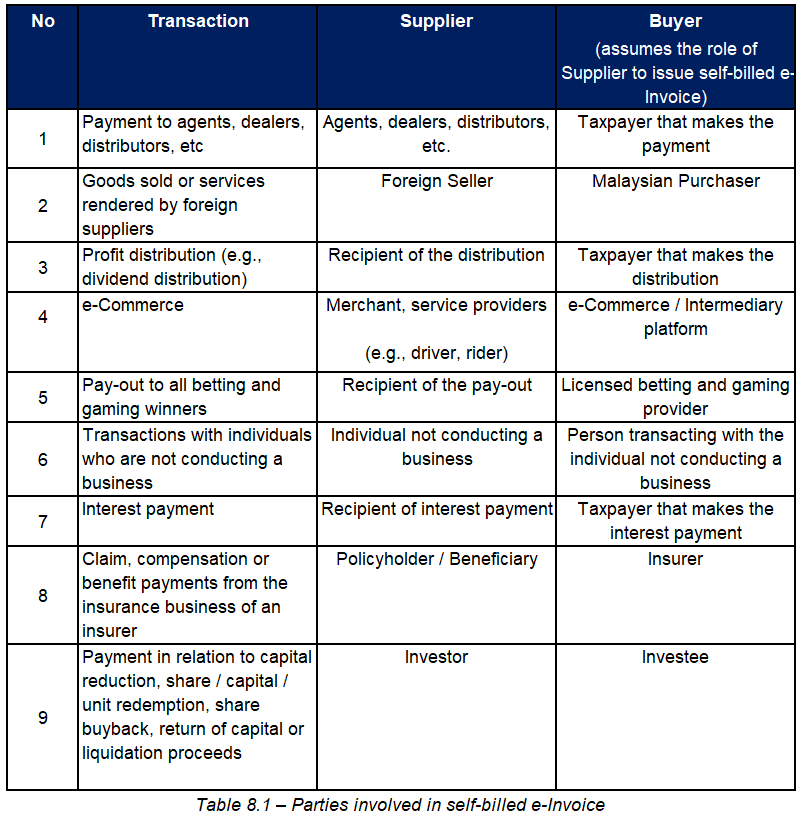

Transactions Requiring Self-Billed E-Invoices:

Payments to agents, dealers, distributors, etc.

Goods sold or services rendered by foreign suppliers.

Profit distribution (e.g., dividends).

E-commerce transactions.

Pay-outs to betting and gaming winners (with some exemptions).

Transactions with individuals not conducting a business.

Interest payments (with specific exceptions).

Claim, compensation, or benefit payments from insurance businesses.

Payments related to capital reduction, share/capital/unit redemption, share buyback, return of capital, or liquidation proceeds.

Timing of Issuance:

If there is a written agreement, the issuance date depends on whether government approval is required.

If there is no written agreement, the issuance date is the date of completion.

Validation and Sharing:

Self-billed e-Invoices must be validated via the MyInvois Portal, which generates a QR code for validation.

Buyers can share either the validated e-Invoice or a visual representation with the supplier.

Parties Involved:

Implementation Timeline:

Taxpayers are allowed until July 1, 2025, to configure their systems for certain requirements.

Remarks:

Table 8.2 – Details of TIN and identification number / passport number to be included by Buyer for issuance of self-billed e-Invoice to individual Supplier

Table 8.3 – Details required to be input by Buyer for issuance of self-billed e-Invoice

-Section End-

Back to Main Menu

Developed by:

Login

Register

Field is required

Username must have at least 1 letters.

Field is required

Password must have at least 6 letters.

Remember me

Forgot password?

Login

Forgot password?

Field is required

Username must have at least 1 letters.

Field is required

Invalid email format.

🇺🇸 +1

🇨🇦 +1

🇰🇿 +7

🇷🇺 +7

🇪🇬 +20

🇿🇦 +27

🇬🇷 +30

🇳🇱 +31

🇧🇪 +32

🇫🇷 +33

🇪🇸 +34

🇭🇺 +36

🇮🇹 +39

🇻🇦 +39

🇷🇴 +40

🇨🇭 +41

🇦🇹 +43

🇬🇧 +44

🇩🇰 +45

🇸🇪 +46

🇳🇴 +47

🇵🇱 +48

🇩🇪 +49

🇵🇪 +51

🇲🇽 +52

🇨🇺 +53

🇦🇷 +54

🇧🇷 +55

🇨🇱 +56

🇨🇴 +57

🇻🇪 +58

🇲🇾 +60

🇦🇺 +61

🇮🇩 +62

🇵🇭 +63

🇳🇿 +64

🇸🇬 +65

🇹🇭 +66

🇯🇵 +81

🇰🇷 +82

🇻🇳 +84

🇨🇳 +86

🇹🇷 +90

🇮🇳 +91

🇵🇰 +92

🇦🇫 +93

🇱🇰 +94

🇲🇲 +95

🇮🇷 +98

🇸🇸 +211

🇲🇦 +212

🇪🇭 +212

🇩🇿 +213

🇹🇳 +216

🇱🇾 +218

🇬🇲 +220

🇸🇳 +221

🇲🇷 +222

🇲🇱 +223

🇬🇳 +224

🇨🇮 +225

🇧🇫 +226

🇳🇪 +227

🇹🇬 +228

🇧🇯 +229

🇲🇺 +230

🇱🇷 +231

🇸🇱 +232

🇬🇭 +233

🇳🇬 +234

🇹🇩 +235

🇨🇫 +236

🇨🇲 +237

🇨🇻 +238

🇸🇹 +239

🇬🇶 +240

🇬🇦 +241

🇨🇬 +242

🇨🇩 +243

🇦🇴 +244

🇬🇼 +245

🇮🇴 +246

🇦🇨 +247

🇸🇨 +248

🇸🇩 +249

🇷🇼 +250

🇪🇹 +251

🇸🇴 +252

🇩🇯 +253

🇰🇪 +254

🇹🇿 +255

🇺🇬 +256

🇧🇮 +257

🇲🇿 +258

🇿🇲 +260

🇲🇬 +261

🇾🇹 +262

🇷🇪 +262

🇿🇼 +263

🇳🇦 +264

🇲🇼 +265

🇱🇸 +266

🇧🇼 +267

🇸🇿 +268

🇰🇲 +269

🇸🇭 +290

🇪🇷 +291

🇦🇼 +297

🇫🇴 +298

🇬🇱 +299

🇬🇮 +350

🇵🇹 +351

🇱🇺 +352

🇮🇪 +353

🇮🇸 +354

🇦🇱 +355

🇲🇹 +356

🇨🇾 +357

🇫🇮 +358

🇧🇬 +359

🇱🇹 +370

🇱🇻 +371

🇪🇪 +372

🇲🇩 +373

🇦🇲 +374

🇧🇾 +375

🇦🇩 +376

🇲🇨 +377

🇸🇲 +378

🇺🇦 +380

🇷🇸 +381

🇲🇪 +382

🇽🇰 +383

🇭🇷 +385

🇸🇮 +386

🇧🇦 +387

🇲🇰 +389

🇨🇿 +420

🇸🇰 +421

🇱🇮 +423

🇫🇰 +500

🇧🇿 +501

🇬🇹 +502

🇸🇻 +503

🇭🇳 +504

🇳🇮 +505

🇨🇷 +506

🇵🇦 +507

🇵🇲 +508

🇭🇹 +509

🇬🇵 +590

🇧🇴 +591

🇬🇾 +592

🇪🇨 +593

🇬🇫 +594

🇵🇾 +595

🇲🇶 +596

🇸🇷 +597

🇺🇾 +598

🇧🇶 +599

🇹🇱 +670

🇳🇫 +672

🇧🇳 +673

🇳🇷 +674

🇵🇬 +675

🇹🇴 +676

🇸🇧 +677

🇻🇺 +678

🇫🇯 +679

🇵🇼 +680

🇼🇫 +681

🇨🇰 +682

🇳🇺 +683

🇼🇸 +685

🇰🇮 +686

🇳🇨 +687

🇹🇻 +688

🇵🇫 +689

🇹🇰 +690

🇫🇲 +691

🇲🇭 +692

🇰🇵 +850

🇭🇰 +852

🇲🇴 +853

🇰🇭 +855

🇱🇦 +856

🇧🇩 +880

🇹🇼 +886

🇲🇻 +960

🇱🇧 +961

🇯🇴 +962

🇸🇾 +963

🇮🇶 +964

🇰🇼 +965

🇸🇦 +966

🇾🇪 +967

🇴🇲 +968

🇵🇸 +970

🇦🇪 +971

🇮🇱 +972

🇧🇭 +973

🇶🇦 +974

🇧🇹 +975

🇲🇳 +976

🇳🇵 +977

🇹🇯 +992

🇹🇲 +993

🇦🇿 +994

🇬🇪 +995

🇰🇬 +996

🇺🇿 +998

🇧🇸 +1242

🇧🇧 +1246

🇦🇮 +1264

🇦🇬 +1268

🇻🇬 +1284

🇻🇮 +1340

🇰🇾 +1345

🇧🇲 +1441

🇬🇩 +1473

🇹🇨 +1649

🇲🇸 +1664

🇲🇵 +1670

🇬🇺 +1671

🇱🇨 +1758

🇩🇲 +1767

🇵🇷 +1787

🇩🇴 +1809

🇩🇴 +1829

🇩🇴 +1849

🇹🇹 +1868

🇰🇳 +1869

🇯🇲 +1876

🇨🇼 +5999

Only numbers

Enable WhatsApp Communication

Field is required

Password must have at least 6 letters.

I accept the

Privacy Policy

You must accept the privacy policy

Register

Compare

{{ props.count }}

Compare

You're almost there, select at least one more listing to compare!